Pork demand has been growing stronger every month and has been phenomenal so far this year. Consumer demand for pork products has helped drive cutout prices higher. There is a lot of talk about short live hog supplies in the industry. But the real issue is stronger pork demand from the consumer, which has been driving pork prices higher in the U.S.

The chart above was assembled with USDA data.

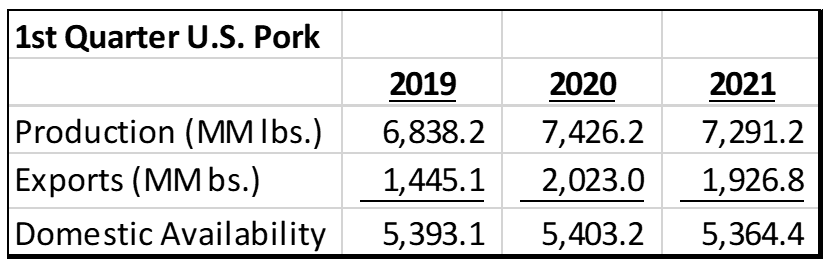

Pork production in the U.S. increased from 2019 to 2020 in the first quarter of the year. Much of this was the high harvest levels before plants shut down due to COVID. Under more normal conditions (if normal exists), harvest levels in 2021 were down from 2020, but production in 2021 was 6.6% higher than 2019. Plentiful production in the first quarter. When comparing 2021 to 2019 again, exports were 33.3% higher in 2021 with continued strong exports to China.

For the quarter, domestic availability was within 0.5% of 2019. No significant change in available pork supplies in the U.S. Price data from USDA shows retail pork prices were up 10.6% in the two-year period. While there are some problems with the retail scanner data, it would show strong prices for retail pork. The problems include not a true “pork expenditure”, which is hard to collect on a broad basis. Also the fact that food-service data is not collected, and much of product goes through non-retail channels.

RELATED: DOES STRENGTH OF THE U.S. DOLLAR IMPACT EXPORTS?

Drivers of the improvement in domestic pork demand likely have much to do with all the stimulus money pumped into the U.S. economy. It will be hard to quantify, but seems reasonable that as disposable income increases, food service and retail meat demand would benefit. We hear a lot about inflation, and the term “commodity super-cycle” more regularly. Time will tell in that regard, but global (insert China) demand for commodities is real and driving our costs of meat production higher. And so far, strong prices are offsetting the costs.

{kind=link}