Live pig prices: The weekly average price of live pigs continued to rise month-on-month this week, mainly due to weak fluctuations.

The price of live pigs continued to rise this week. Jilin was 7.80-8.10 yuan/catties, an increase of 0.16 yuan/catties from last week, and Liaoning was 7.80-8.10 yuan/catties, an increase of 0.12/kg from last week. Beijing is at 8.30-8.60 yuan/jin, an increase of 0.18 yuan/jin from last week. Zhejiang is at 9.20-9.50 yuan/catties, up 0.21 yuan/kg from last week. Xinjiang is 7.60-7.90 yuan/catties, up 0.20 yuan/kg from last week. Sichuan rose to 9.20-9.50 yuan/catties, Hebei rose to 8.30-8.60 yuan/catties, Shandong rose to 8.40-8.70 yuan/catties, Henan rose to 8.50-8.80 yuan/catties, and Guangdong rose to 9.30-9.60 yuan/catties.

Pork prices: The Ministry of Commerce monitors the increase in the wholesale price of white striped pigs in the second week of November. Pork prices continue to rise, but the increase has narrowed compared to last week. After the price of pork rose, the acceptance at the retail end declined, the delivery of white strips slowed down, and the price of pork stagnated.

Piglet prices: Monitoring data from the Ministry of Agriculture and Rural Affairs showed that piglet prices rose by 4.40% month-on-month last week and fell by 70.10% from the same period last year. The average piglet price in 500 rural markets across the country was RMB 25.85/kg. According to statistics from this website, the price of piglets in yuan rose to RMB 20.81/kg this Wednesday, and the price of piglets continued to rise this week. Farmers’ replenishment increased as the price of pigs rose, but overall the supply of piglets was sufficient.

The price of pig food: pig food rose to 6.38 this week, an increase of 0.18 compared to last week. The price of corn was 2.76 yuan/kg, an increase of 0.02 yuan/kg from last week. This week’s self-reproduction and self-support loss was 21.20 yuan/head, a decrease of 71.85 yuan/head from last week’s loss. After rain and snow, the temperature has picked up, new corn fever and mold in the main domestic production areas have increased, and it is difficult for grassroots growers to store it. Traders such as drying towers are more cautious in building warehouses. The market circulation remained high, suppressing the weak price market. The winter of the main corn producing areas in northern China this year came earlier than previous years. The new season corn encountered strong snowfall at the end of the harvest, which superimposed logistics delays, which further delayed the increase of new grains. It is expected that corn prices will continue to be moderately biased in most of November. The strong trend is the main trend. After the second half of the year, as the supply of corn further increases, there is a chance for its price to weaken.

Market summary: The weekly average price of live pigs continued to rise this week, and the price showed a downward trend during the week. After the increase in pork prices, downstream consumers’ enthusiasm for pork consumption has cooled, and their resistance has increased. After the residents responded to the call to stock food and meat, the purchasing power of fresh meat has also indirectly decreased, and the enthusiasm of traders to get the goods has also declined, and slaughter companies Baitiao’s delivery speed slowed down. In addition, there are still a lot of frozen pork stocks in the market, which will continue to be exported in the near future. The overall supply of pork is sufficient. The increase in pork prices is not as high as the increase in the price of pigs. This limits the increase in the price of pigs. The pig price formed support. It is expected that the forecast of pig prices in November-December will be mainly volatile and strong, and there may be frequent fluctuations during this period.

In addition, according to data released by the Ministry of Agriculture and Rural Affairs, the national stock of reproductive sows at the end of October was 43.48 million, a decrease of 2.49% from September. The number of reproductive sows has declined for three consecutive months, and the national stock of reproductive sows continues to be orderly. The reduction, but still 6% more than the normal holding of 41 million heads, is expected to be adjusted to an appropriate level in the first quarter of next year.

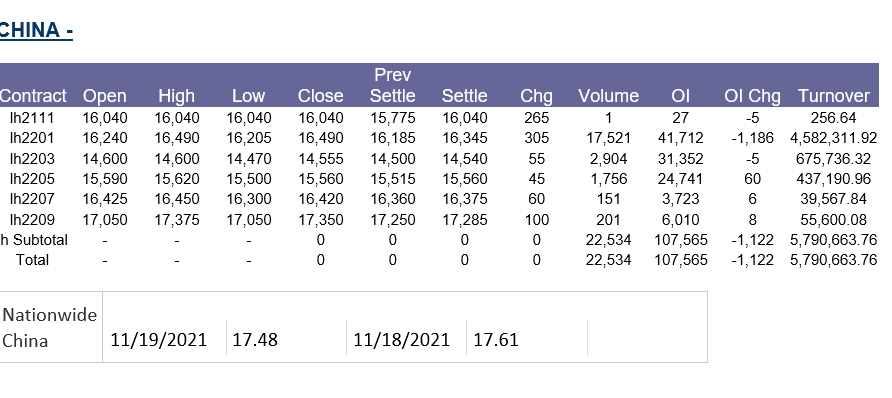

source: feedtrade

Trading futures, Options on Futures and retail off-exchange foreign currency transaction involves substantial risk of loss and is not suitable for all investors you would consider whether trading is suitable for you in light of your circumstances, knowledge, and financial resources. You may lose all or more than your initial investment. Options, Market data, and recommendations are subject to change without notice. Past Performance is not necessarily indicative of future results.

{kind=link}